what is a deferred tax provision

The deferred tax represents the negative or positive amounts of tax owed by the Company. Deferred tax refers to income tax overpaid or owed due to the temporary differences between accounting income and taxable income.

Cacique Accounting College Today S Topic Acca P2 Corporate Reporting Deferred Tax A Deferred Tax Liability Is An Account On A Company S Balance Sheet That Is A Result Of

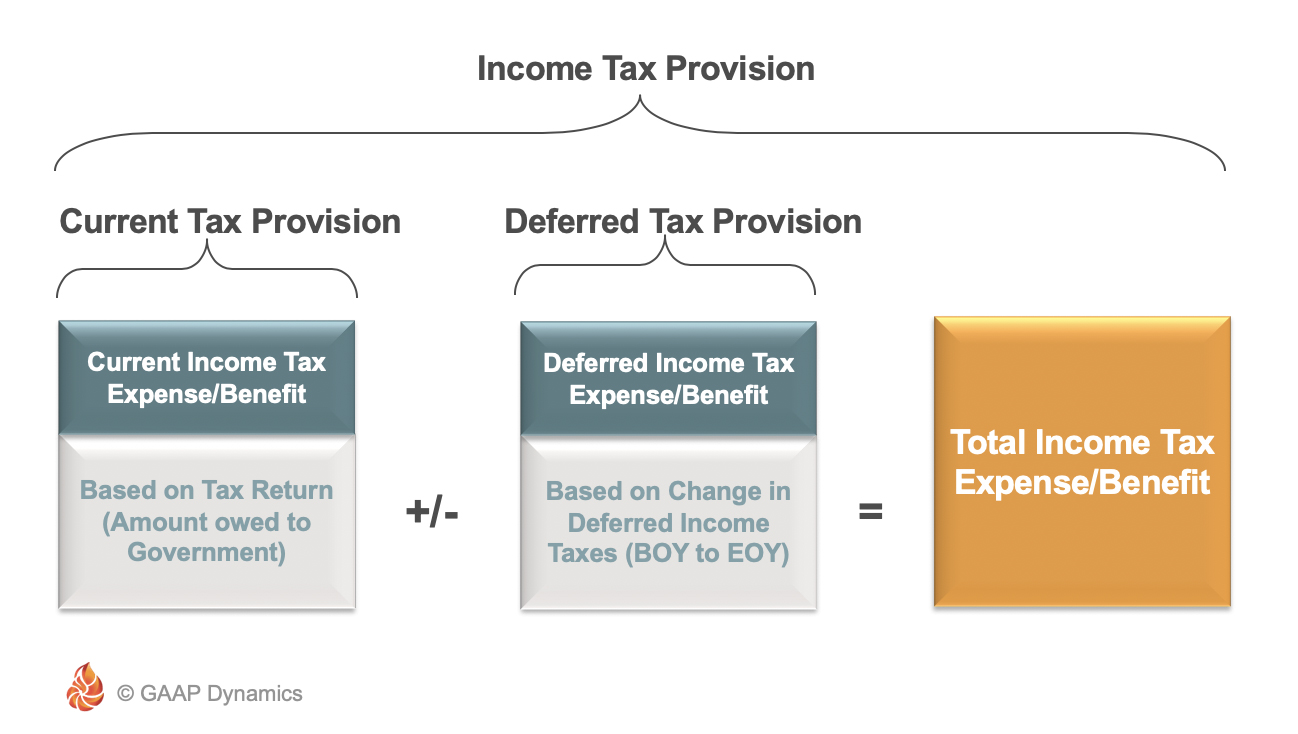

To estimate the current income tax provision.

/dotdash_Final_Deferred_Tax_Asset_Definition_Aug_2020-01-dab264b336b94f939b132c55c018f125.jpg)

. Deferred tax liabilities and deferred tax assets. Depreciation on fixed assets. In year 1 they buy a computer for 1800 and this is written off in the accounts by way of a.

Thus the Company will have to pay tax on 10500 creating this tax asset. However in its tax statements it has not mentioned that provision due to which their gross profit is Rs. A deferred tax liability is an account on a companys balance sheet that is a result of temporary differences between the companys accounting and tax carrying values the.

Provision on doubtful accounts or debt or warranty. Deferred income tax expense. However this bad debt is not considered for taxes until it has been written off.

Lets assume that a company has a book profit of 10000 for a financial year including a provision of 500 as bad debt. Generally FRS 102 adopts a timing difference approach. Therefore it cannot be based on a fair value of an asset that is measured at cost in the statement of financial position.

Deferred Income Tax. The deferred income tax is a liability that the company has on its balance sheet but that is not due for payment yet. A deferred income tax is a liability recorded on the balance sheet that results from a difference in income recognition between tax laws and accounting methods.

The term deferred tax refers to a tax which shall either be paid in future or has already been settled in advance. Deferred tax income for current year 5000 5000-0 The company profit before tax is 80000. It is part of the accounting adjustment and gets eliminated as the temporary differences are reversed over time.

Deferred tax is a balance sheet line item which is recorded because the Company owes or pay more tax to the authorities. Add or subtract the net change in temporary differences. However it is the profit in accounting base so we have to make adjustment to determine taxable income by adding 20000 as revenues in 2017.

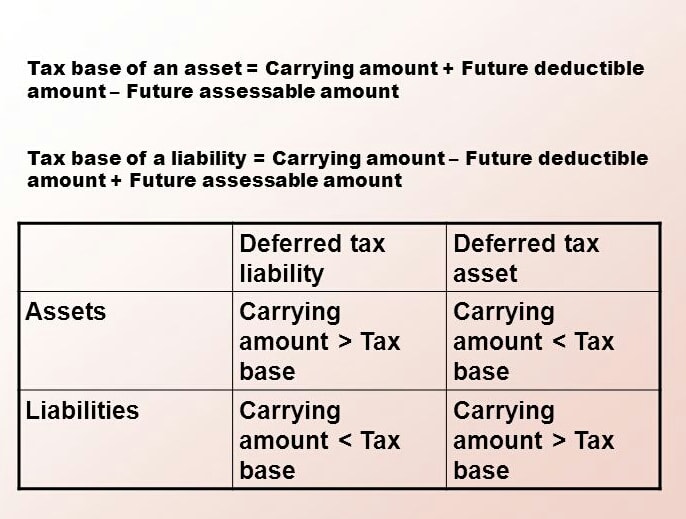

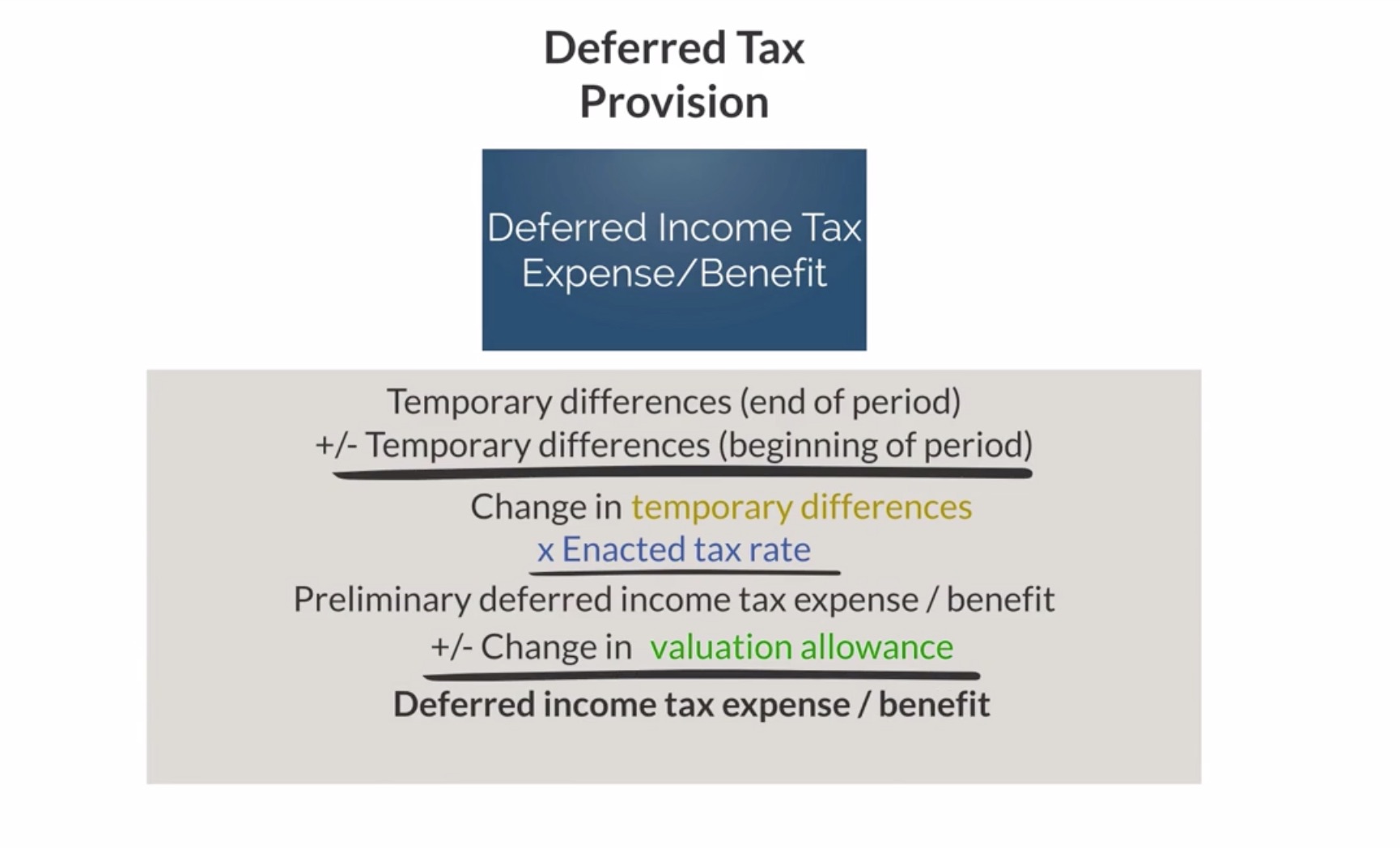

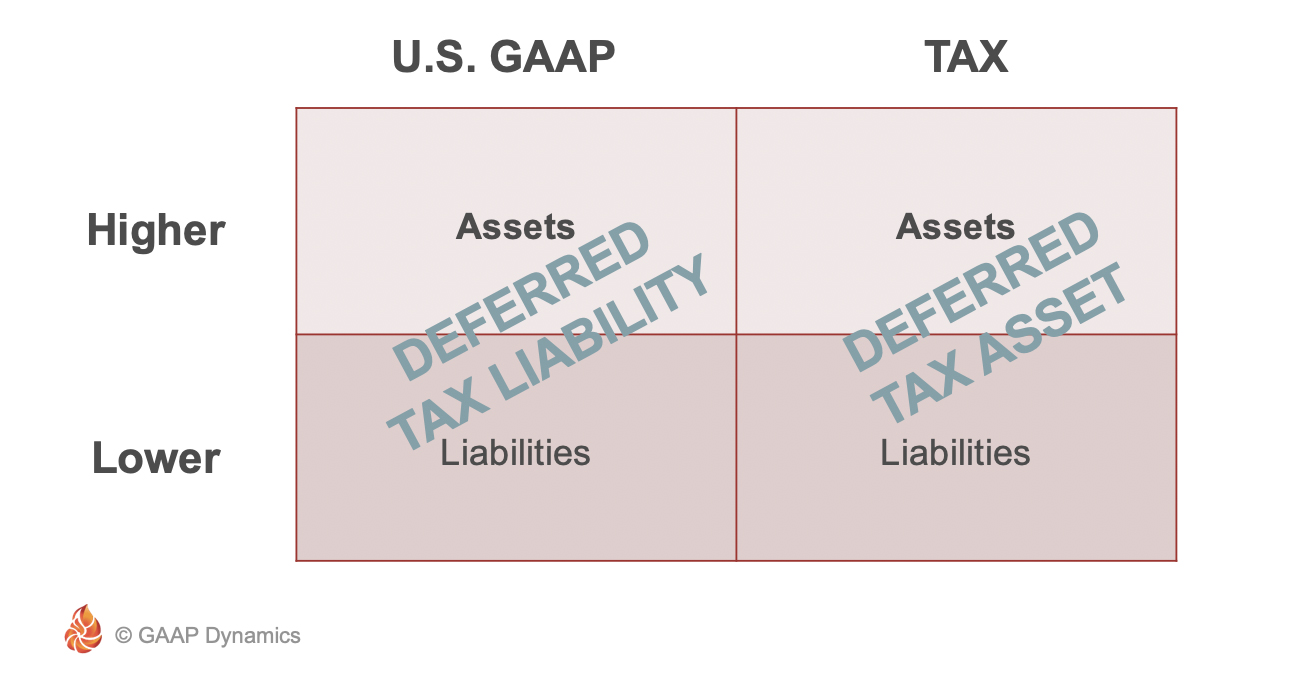

A deferred tax often represents the mathematical difference between the book carrying value ie an amount recorded in the accounting balance sheet for an asset or liability and a corresponding tax basis determined under the tax laws of that jurisdiction in the asset or liability multiplied by the applicable jurisdictions statutory. Deferred income taxes impact the future cash flow of the Company ie if its an asset the cash outflow will be less and. The result is your companys current year tax expense for the income tax provision.

Add or subtract net permanent differences. In this article we will see why a company may differ its tax to a subsequent fiscal year or why a company may choose to pay the tax in advance. Subtract usable loss carryforwards.

The deferred income tax is a charge on the balance sheet of the company but is not required to be repaid. Calculating the cumulative total of all temporary differences using the appropriate tax rates is part of the income tax provisions more complicated section. Lets look at an example.

Deferred Tax Liability. Another example of Deferred tax assets is Bad Debt. Start with pretax GAAP income.

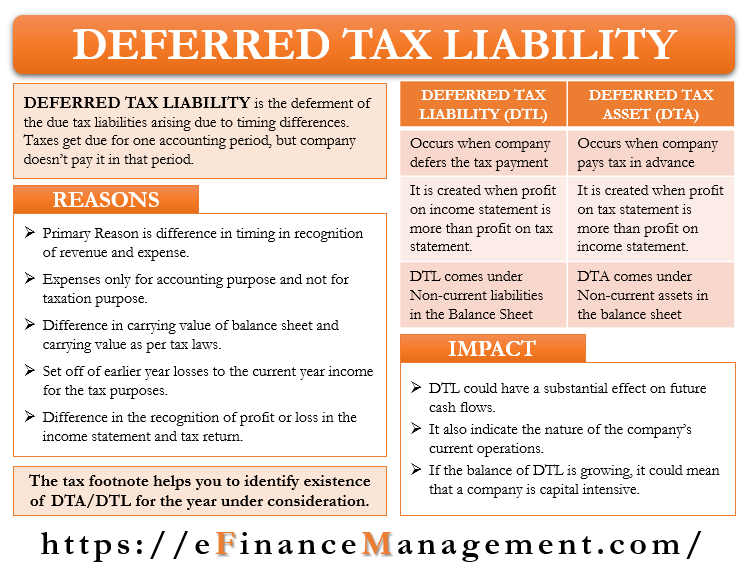

Both will appear as entries on a balance sheet and represent the negative and positive amounts of tax owed. A provision is created when deferred tax is charged to the profit and loss account and this provision is reduced as the timing difference reduces. Deferred tax is a topic that is consistently tested in Financial Reporting FR and is often tested in further detail in Strategic Business Reporting SBR.

Deferred tax is the amount of tax payable or recoverable in future reporting periods as a result of transactions or events recognised in current or previous periods accounts. It is recorded as a liability or asset in the balance sheet at the year-end. Note that there can be one without the other - a company can have only deferred tax liability or deferred tax assets.

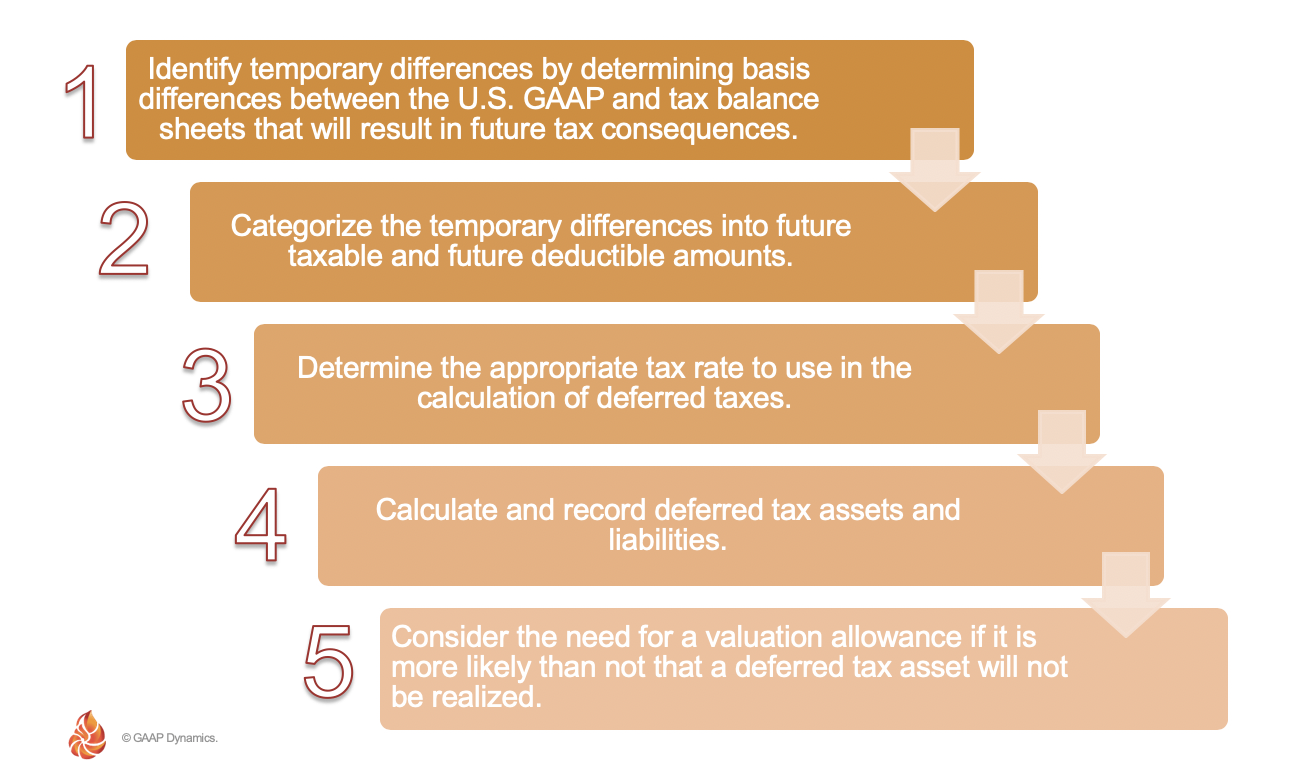

This more complicated part of the income tax provision calculates a cumulative total of the temporary differences. Decrease the book profit by the amount of deferred tax if at all such an amount appears on the credit side of the profit and loss account. This article Deferred tax provisions 123 kb sets out four key areas of your tax provision that could be affected by the impacts of COVID-19.

Deferred tax is a notional asset or liability to reflect corporate income taxation on a basis that is the same or more similar to recognition of profits than the taxation treatment. Deferred tax assets and liabilities are not discounted IAS 1253-54. Therefore it is creating a deferred tax asset of Rs.

Multiply the result by. Income Tax Slab Tax Rates for FY 2021-22 AY 2022-23. It is important to use the right version and to make sure that it applies to the.

Increase the book profit by the amount of deferred tax and its provision or. The measurement of deferred tax is based on the carrying amount of the assets and liabilities of an entity IAS 1255. The deferred income tax expense calculates the sum total of the temporary differences and applies the federal corporate tax rate to the resulting.

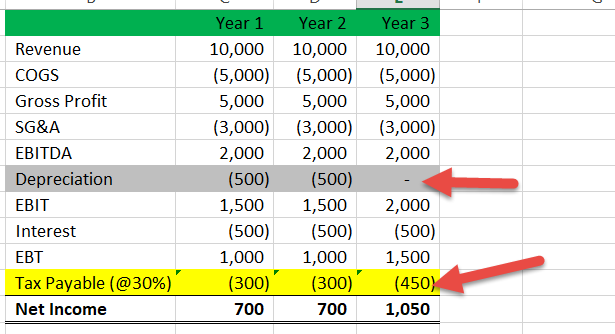

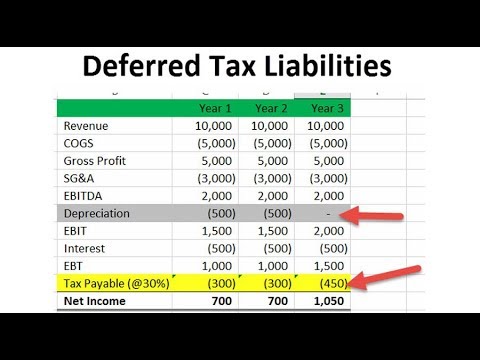

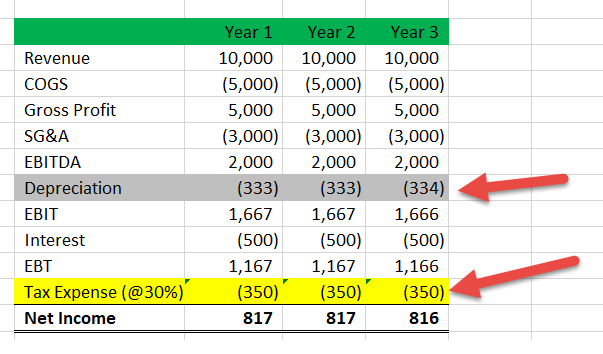

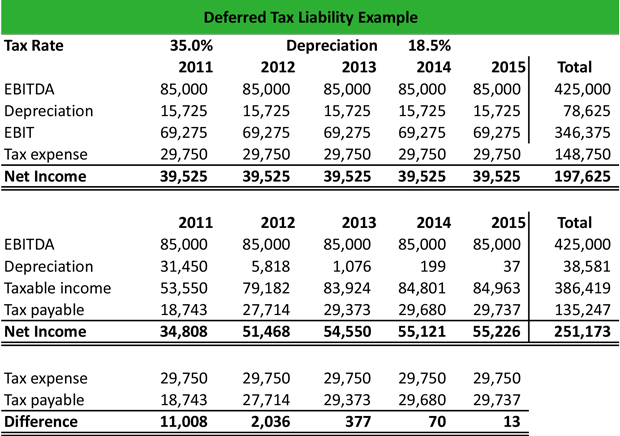

Its also a result of the differences in income recognition between income tax accounting rules and your companys accounting. Deferred tax can fall into one of two categories. A business has profits each year of 5000 before any depreciation charge.

This article will start by considering aspects of deferred tax that are relevant to FR before moving on to the more complicated situations that may be tested in SBR. Most companies normally prepare an income statement and a tax statement every. Definition of Deferred Tax.

More specifically we focus on how government support in the form of tax incentives and tax relief might change previous assessments that were made applying IAS 12 Income Taxes IAS 12. Deferred tax liabilities can arise as a result of corporate taxation treatment of capital expenditure being more rapid than the accounting depreciation treatment. Deferred tax is the tax that is levied on a company that has either been deducted in advance or is eligible to be carried over to the succeeding financial years.

Deferred income tax expense is the opposite of deferred tax assets.

Deferred Tax Asset Deferred Tax Assets Vs Deferred Tax Liability

/dotdash_Final_Deferred_Tax_Asset_Definition_Aug_2020-01-dab264b336b94f939b132c55c018f125.jpg)

Deferred Tax Asset Definition

Accounting For Income Taxes Under Asc 740 An Overview Gaap Dynamics

:max_bytes(150000):strip_icc()/dotdash_Final_Deferred_Tax_Asset_Definition_Aug_2020-01-dab264b336b94f939b132c55c018f125.jpg)

Deferred Tax Asset Definition

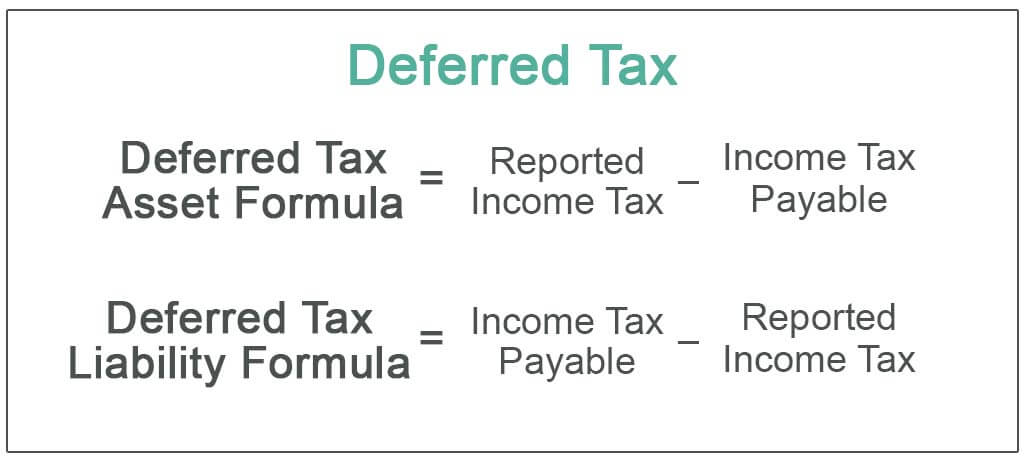

Deferred Tax Liabilities Meaning Example How To Calculate

Deferred Tax Liabilities India Dictionary

Accounting For Income Taxes Under Asc 740 Deferred Taxes Gaap Dynamics

Worked Example Accounting For Deferred Tax Assets The Footnotes Analyst

Accounting For Income Taxes Under Asc 740 Deferred Taxes Gaap Dynamics

Deferred Tax Liabilities Meaning Example How To Calculate

Define Deferred Tax Liability Or Asset Accounting Clarified

Net Operating Losses Deferred Tax Assets Tutorial

Deferred Tax Meaning Expense Examples Calculation

What Is A Deferred Tax Liability Community Tax

Deferred Tax Asset Definition

Accounting For Income Taxes Under Asc 740 Deferred Taxes Gaap Dynamics

What Is A Deferred Tax Liability Dtl Definition Meaning Example

Deferred Tax Liabilities Meaning Example Causes And More

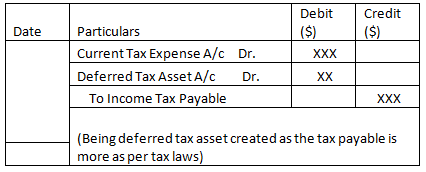

Deferred Tax Double Entry Bookkeeping